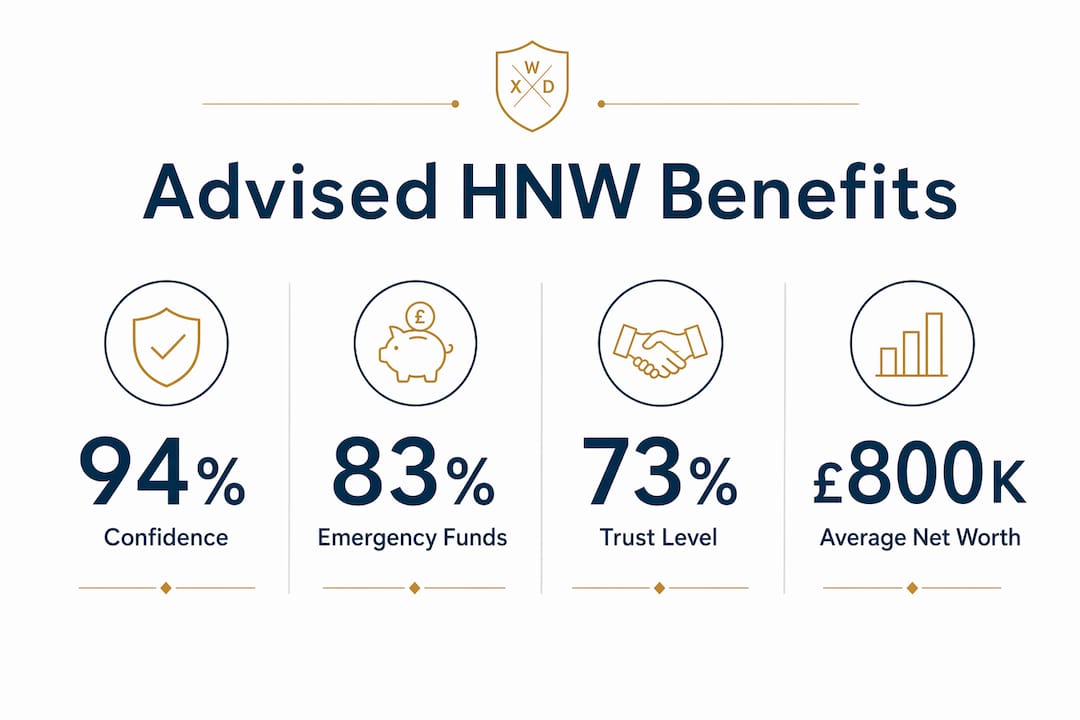

High-net-worth (HNW) wealth management is defined as the coordinated management of complex assets, tax structures, legal arrangements, and lifestyle needs that exceed the scope of standard financial planning. The case for why HNW individuals need advisors is not theoretical. Advised households report an average net worth of £800,000, more than double non-advised households at £388,000, even after adjusting for income and demographics. That gap does not appear by accident. It reflects the compounding effect of better decisions, fewer costly errors, and coordinated planning across every dimension of wealth.

Why HNW individuals need advisors: what makes it different?

HNW financial planning is fundamentally distinct from standard approaches because the scale of assets changes the nature of every decision. A poorly structured trust, a missed tax window, or a badly timed liquidity event can each cost more than years of advisory fees. A single advisory error in trusts or tax planning can exceed the total cost of professional advice at HNW level. That asymmetry is the core argument for specialist guidance.

Concentration risk is one of the most common and underappreciated dangers. Many HNW families hold a large proportion of their wealth in a single business, property, or inherited shareholding. Diversifying that position without triggering a significant tax liability requires specialist knowledge, not general financial advice. The same applies to illiquid assets such as private equity stakes, art collections, or aviation assets, where valuation, insurance, and exit planning each require dedicated expertise.

Generational planning adds another layer of complexity. Transferring wealth across generations involves inheritance tax planning, trust structures, family governance, and, increasingly, preparing heirs to manage what they receive. Each of these areas touches a different professional discipline. Without a central coordinator, the advice from a solicitor, an accountant, and an investment manager can pull in different directions without anyone noticing.

The fiduciary standard matters here. An advisor operating under a fiduciary duty is legally obligated to act in the client’s best interests, not their own. That standard is not universal across the advisory industry. HNW clients who do not verify this distinction risk working with advisors who have their hand in the client’s till through commissions, referral fees, or product incentives. Bespoke wealth management at HNW level demands fiduciary commitment as a baseline, not a bonus.

Pro Tip: Before engaging any advisor, ask directly whether they operate under a fiduciary standard and confirm they receive no referral fees or product commissions. If they hesitate, that is your answer.

How do advisors add value beyond investment management?

The most significant advisory value often has nothing to do with markets. Advisors provide their greatest value during non-market events such as life transitions, family disputes, and unexpected liquidity events, where objective decision-making prevents costly emotional errors. A divorce, a business sale, or the death of a family member each triggers financial consequences that require calm, expert coordination under time pressure.

The role of an advisor as a central coordinator is what separates effective HNW planning from fragmented advice. Fragmentation risk is the primary challenge for modern HNW families, where the lack of coordination among tax, estate, investment, and governance advisors creates gaps that cost money and create legal exposure. A skilled lead advisor prevents that fragmentation by ensuring every professional on the team is working from the same plan.

The breadth of advisory value for HNW clients extends well beyond portfolio returns:

- Estate planning coordination. Advisors work alongside solicitors to structure wills, trusts, and lasting powers of attorney in a way that aligns with the overall wealth plan, not just legal compliance.

- Philanthropy and charitable giving. Structured giving through vehicles such as charitable remainder trusts can reduce tax liability while achieving meaningful philanthropic goals.

- Insurance gap analysis. Many HNW families are significantly underinsured against liability, particularly for high-value properties, vehicles, and personal liability claims.

- Liquidity event preparation. A business sale or inheritance requires advance planning across tax, investment, and legal disciplines simultaneously.

- Lifestyle asset management. Aircraft, classic cars, watches, and art each carry insurance, maintenance, and valuation obligations that require specialist oversight.

Pro Tip: Ask your advisory team to map every professional involved in your financial affairs and identify who is responsible for coordinating between them. If no one owns that role, you have a fragmentation problem.

What are the measurable benefits reported by advised HNW households?

The data on advised versus non-advised outcomes is consistent and compelling. 94% of CFP-advised households feel confident in achieving their financial goals, compared to 81% for those without an advisor. That confidence gap reflects real differences in preparedness, not just perception.

Emergency fund discipline is one concrete measure. Among CFP-advised households, 83% maintain a three-month emergency fund, compared to 53% for non-advised households. For HNW clients, the equivalent is maintaining adequate liquidity buffers across illiquid portfolios, a discipline that requires active planning rather than good intentions.

Trust and satisfaction levels also differ sharply. Clients working with CFP professionals report stronger trust at 73% versus 52%, higher satisfaction at 62% versus 44%, and measurably reduced financial anxiety. For HNW clients managing complex, multi-generational wealth, that reduction in anxiety has a direct impact on decision quality.

| Metric | Advised households | Non-advised households |

|---|---|---|

| Average net worth | £800,000 | £388,000 |

| Confidence in financial goals | 94% | 81% |

| Maintain 3-month emergency fund | 83% | 53% |

| Trust in their advisor | 73% | 52% |

| Satisfaction with financial outcomes | 62% | 44% |

The pattern across every metric points in the same direction. Professional advisory services for HNW clients do not just improve returns. They improve the entire financial experience, from preparedness to peace of mind.

What practical strategies do specialised advisors use to protect HNW wealth?

Specialist advisors deploy specific tools and structures that are simply not available or appropriate at lower wealth levels. Vehicles such as 10b5-1 plans, exchange funds, and charitable remainder trusts allow HNW clients to diversify concentrated positions with tax efficiency. Each of these requires specialist legal and tax knowledge to implement correctly.

Insurance is one of the most overlooked areas of HNW wealth protection. Umbrella insurance policies costing roughly £400 to £1,000 annually are frequently overlooked by HNW families, leaving multimillion-pound estates exposed to personal liability claims. A single lawsuit without adequate coverage can erode decades of wealth accumulation. Specialist advisors identify and close these gaps as a matter of routine.

The annual multidisciplinary meeting is one of the most practical and underused tools in HNW planning. Annual joint meetings among estate attorneys, CPAs, and advisors prevent costly misalignments and keep complex wealth plans coordinated. Without this structure, professionals working in silos make decisions that contradict each other, often without anyone realising until the damage is done.

Proactive estate planning is particularly urgent given the pace of legislative change. Tax laws affecting inheritance, trusts, and wealth transfer shift regularly, and strategies that were effective three years ago may now create liability. Advisors who specialise in estate planning for new wealth monitor these changes and update client structures before problems arise, not after.

Key takeaways

HNW individuals who work with specialist advisors consistently accumulate more wealth, report greater confidence, and avoid the costly errors that fragmented or uncoordinated advice produces.

| Point | Details |

|---|---|

| Advised households accumulate more | Advised households report average net worth more than double that of non-advised households. |

| Fragmentation is the primary risk | Lack of coordination across tax, estate, and investment advice creates costly gaps for HNW families. |

| Advisory value peaks at non-market events | Life transitions and family disputes are where objective, expert guidance prevents the most expensive errors. |

| Specialist tools require specialist knowledge | Vehicles like 10b5-1 plans and charitable remainder trusts require legal and tax expertise to implement correctly. |

| Insurance gaps are a hidden liability | Umbrella policies costing under £1,000 annually protect estates worth millions from personal liability exposure. |

Why I believe coordination is the real product

Having worked with HNW families across a range of financial and lifestyle circumstances, the pattern I see most often is not bad investment performance. It is fragmentation. A client has a solicitor, an accountant, an investment manager, and an insurance broker, each doing competent work in isolation, but no one is talking to anyone else. The result is a plan with gaps, contradictions, and missed opportunities that none of the individual advisors can see from their own vantage point.

The most valuable thing a specialist advisor does is own the whole picture. That means reading the estate plan alongside the investment strategy, checking whether the insurance coverage reflects the current asset base, and asking the questions that fall between professional disciplines. Most costly mistakes I have seen were not caused by bad advice in any single area. They were caused by good advice in one area that conflicted with good advice in another, with no one coordinating between them.

I am also direct about the advisory industry’s conflicts of interest. Too many advisors are paid through commissions or referral fees that create incentives misaligned with the client’s interests. HNW clients deserve advisors who are paid by them, not by the products they recommend. Vetting advisors independently before engagement is not optional at this level of wealth. It is the first act of good financial governance.

The clients I have seen thrive are those who treat their advisory team as a coordinated unit, not a collection of specialists they call one at a time. That shift in approach, from transactional to relational, from siloed to coordinated, is where the real value of advisory services for HNW clients lives.

— Alex Goldstein

How NXD Family Office serves complex HNW needs

NXD Family Office was built specifically for clients whose wealth demands more than a single advisor can provide. The team coordinates across tax, estate planning, investment, insurance, and lifestyle assets, acting as the central point of accountability that most HNW families are missing.

Every client relationship at NXD Family Office is built on unbiased advice, with no referral fees or commissions influencing any recommendation. The wealth management services cover the full spectrum of HNW needs, from structuring complex portfolios to securing access to rare experiences that money alone cannot arrange. Whether you are managing a liquidity event, planning a generational transfer, or simply want one trusted team coordinating every aspect of your financial life, NXD Family Office delivers. Consider it done.

FAQ

What is the main reason HNW individuals need specialist advisors?

HNW wealth involves concentrated assets, complex tax structures, and multi-generational planning that standard financial advice does not address. A single error in trust or tax planning can cost more than years of advisory fees.

How much more do advised households accumulate compared to non-advised?

Advised households report an average net worth of £800,000, more than double the £388,000 reported by non-advised households, even after adjusting for income and demographics.

What does fragmentation risk mean for HNW families?

Fragmentation risk is the danger that arises when tax, estate, investment, and governance advisors work in silos without coordination. The gaps between their advice create costly errors that no single advisor can see.

Why is umbrella insurance important for HNW clients?

Umbrella liability policies costing roughly £400 to £1,000 annually protect multimillion-pound estates from personal liability claims. Many HNW families overlook this cover entirely, leaving significant assets exposed.

What should HNW clients look for when choosing an advisor?

Clients should confirm that any advisor operates under a fiduciary standard and receives no commissions or referral fees. Working with independent advisors who are paid directly by the client removes the most common conflicts of interest.