Financial independence planning is defined as the process of organising your finances to build sufficient wealth that covers your living expenses without relying on employment income. Known in professional circles as FI planning, it draws on budgeting, saving, investing, and debt management to create a portfolio that works for you rather than the other way around. Two concepts sit at the heart of every FI plan: the FI number, which is the total portfolio size you need, and the 4% withdrawal rule, which determines how much you can safely spend each year. Get these right and you gain something most people never achieve: genuine financial freedom and the flexibility to choose how you spend your time.

What is financial independence planning and why does it matter?

Financial independence planning is the strategic management of your finances to generate enough passive income to support your lifestyle without work. The importance of financial independence extends well beyond retirement. It removes financial stress, gives you negotiating power in your career, and lets you make decisions based on preference rather than necessity.

The financial planning basics that underpin FI planning are straightforward. You track what comes in, control what goes out, grow the difference, and protect what you build. The challenge is doing all four consistently over years or decades, which is why structure and discipline matter more than income level alone.

High-net-worth individuals face a specific version of this challenge. Complex asset structures, tax obligations, lifestyle costs, and estate considerations all interact. A plan that works for someone with a £50,000 salary looks nothing like one built for an entrepreneur with multiple income streams, property holdings, and a family to provide for.

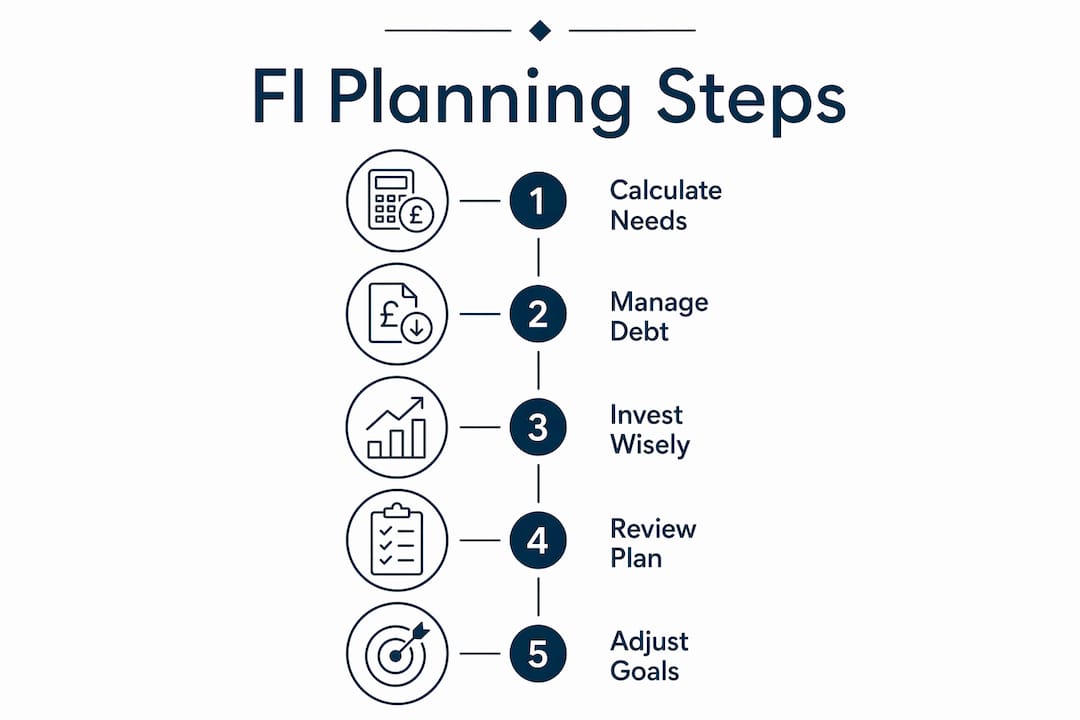

What are the essential components of financial independence planning?

Budgeting and expense tracking form the foundation of any credible FI plan. Without a clear picture of your cash flow, every other decision is guesswork. Careful monitoring of spending reveals where money leaks and where savings can be redirected toward wealth-building.

The core components of a sound FI plan are:

- Emergency fund: An emergency fund covering 3–6 months of expenses protects against unexpected setbacks and prevents you from raiding investments or taking on debt during a crisis.

- Debt management: High-interest debt destroys wealth faster than most investments can build it. Prioritise clearing it before aggressively investing.

- Investing for growth: Tax-advantaged accounts and low-cost index funds grow assets over time while reducing tax drag. This is the engine of FI.

- Clear financial goals: Measurable targets, such as a specific FI number or a target retirement date, give your plan direction and allow you to track progress.

- Regular reviews: Life changes. Markets move. A plan that is never revisited becomes obsolete.

Pro Tip: Set a calendar reminder every six months to review your FI plan. Even a 30-minute review catches drift before it becomes a problem.

Debt management deserves particular attention. Many people focus entirely on investment returns while carrying expensive debt. A credit card charging 20% annually is a guaranteed 20% return when you pay it off. No index fund offers that certainty.

How is the financial independence number calculated?

The FI number is a personalised target that accounts for your expenses, lifestyle, inflation, and how long your assets need to last. It is not a fixed amount. It connects expected income sources and assumptions to define exactly how much wealth you need before work becomes optional.

The most widely used method is the 25x rule, which is directly linked to the 4% withdrawal rule. William Bengen’s 1994 research, published in the Journal of Financial Planning, established that a retiree can withdraw 4% of their portfolio in year one and adjust for inflation each subsequent year without running out of money over a 30-year period. Multiply your annual expenses by 25 and you have your FI number.

The table below shows how FI numbers scale with annual spending:

| Annual Expenses | FI Number (25x Rule) | Monthly Investment Needed (Approx.) |

|---|---|---|

| £30,000 | £750,000 | £1,200 |

| £60,000 | £1,500,000 | £2,400 |

| £100,000 | £2,500,000 | £4,000 |

| £150,000 | £3,750,000 | £6,000 |

| £250,000 | £6,250,000 | £10,000 |

Monthly investment figures are illustrative, assuming 7% annual growth over 25 years.

Three factors shift your FI number significantly. Lifestyle inflation pushes it higher. A higher expected investment return lowers it. Retiring earlier extends the withdrawal period and demands a larger buffer. For high-net-worth clients, private schooling, property maintenance, and luxury lifestyle costs can add hundreds of thousands to the target figure.

Pro Tip: Use a compound interest calculator such as those available through MoneySavingExpert or the MoneyHelper website to model different savings rates and timelines. Small changes in your savings rate produce dramatic differences over 20 years.

What practical steps accelerate achieving financial independence?

Increasing your savings rate reduces your timeline to FI more than income level alone. The gap between what you earn and what you spend is the single most powerful variable in your plan. Widening that gap by even 5% can shave years off your timeline.

The steps to financial independence that consistently deliver results are:

- Track every expense for 90 days. You cannot manage what you do not measure. Most people are surprised by where money actually goes once they look closely.

- Set a target savings rate. Aim for at least 20%, though many serious FI planners target 40–50%. The higher the rate, the faster the timeline compresses.

- Invest consistently in low-cost index funds. Vanguard, iShares, and similar providers offer diversified exposure at minimal cost. Consistency beats timing every time.

- Maximise tax-advantaged accounts. In the UK, ISAs and SIPPs shelter returns from tax and compound growth more efficiently. Use the full annual allowances before investing in taxable accounts.

- Reinvest all returns. Compound growth requires that dividends and gains are reinvested rather than spent. This is non-negotiable in the accumulation phase.

- Adapt the plan for life changes. A pay rise, inheritance, property purchase, or new dependent all change the numbers. Review and adjust rather than assuming the original plan still holds.

The tax advisory services available to high-net-worth individuals can make a material difference here. Structuring investments tax-efficiently is not a luxury. For someone with a £2 million portfolio, the difference between a 0.5% and a 2% annual tax drag compounds to hundreds of thousands of pounds over a decade.

What challenges should you anticipate in FI planning?

Inflation is retirees’ greatest enemy, according to William Bengen himself. The 4% rule applies only in the first year of retirement. Every subsequent year, the withdrawal amount must increase in line with inflation to maintain purchasing power. A plan that ignores this erodes living standards quietly but relentlessly.

The most common challenges in FI planning are:

- Sequence of returns risk: A market downturn in the first years of retirement can permanently damage a portfolio, even if long-term returns recover. Holding 1–2 years of expenses in cash or short-term bonds reduces this risk.

- Underestimating lifestyle costs: Many people plan for a frugal retirement and then discover they do not want one. Build in a realistic lifestyle budget, including travel, health, and family support.

- Ignoring tax implications: Withdrawals from pensions, property sales, and investment accounts all carry tax consequences. Estate planning and accountancy services should be part of the plan from the outset.

- Failing to stress-test the plan: Regular reviews and stress-testing for market downturns, unexpected expenses, and liquidity events are critical for a resilient FI strategy. A plan that has never been tested under pressure is not a plan. It is a wish.

Working optionality is a nuance that many FI planners overlook. Reaching your FI number does not mean you must stop working. Many people choose to continue in some capacity, which reduces withdrawal pressure and extends portfolio longevity. Building this flexibility into your plan from the start gives you more options, not fewer.

Key takeaways

Financial independence planning requires a clear FI number, a disciplined savings rate, tax-efficient investing, and a plan that is stress-tested and reviewed regularly.

| Point | Details |

|---|---|

| Define your FI number | Multiply annual expenses by 25 to set a clear, measurable wealth target. |

| Prioritise savings rate | Increasing the gap between income and spending accelerates FI faster than chasing returns. |

| Invest tax-efficiently | Use ISAs, SIPPs, and low-cost index funds to reduce tax drag and compound growth faster. |

| Plan for inflation | Adjust withdrawals annually for inflation to protect purchasing power throughout retirement. |

| Stress-test regularly | Review and test your plan every six months to account for life changes and market conditions. |

Why most FI plans fail before they start

I have worked with enough high-net-worth clients to know that the biggest obstacle to financial independence is not a lack of money. It is a lack of structure. People arrive with significant assets, strong income, and no coherent plan. They have been told by advisors who earn commission on product sales that they are “on track,” but nobody has ever sat down and calculated their actual FI number or modelled what inflation does to their lifestyle over 30 years.

The one-size-fits-all approach that dominates traditional financial advisory is, frankly, inadequate for anyone with complex finances. A generic pension contribution and a balanced fund is not a financial independence strategy. It is a placeholder.

What I have seen work, consistently, is a combination of three things: a precise FI number built on honest lifestyle assumptions, a tax structure that does not leak wealth unnecessarily, and a plan that is reviewed with the same rigour as a business. The clients who achieve genuine financial freedom are not always the wealthiest. They are the most disciplined and the best advised.

The other mistake I see repeatedly is neglecting debt management in the accumulation phase. Carrying expensive debt while investing is mathematically incoherent. Yet it is remarkably common. Sort the debt first. Then invest with full force.

How Nxdfamilyoffice supports your path to financial independence

Nxdfamilyoffice works with high-net-worth individuals and families who want a financial independence plan built around their actual life, not a generic template. The approach is straightforward: unbiased advice, no referral fees, no commissions, and no advisors with their hand in the till.

Whether you are calculating your FI number for the first time, restructuring a complex portfolio, or planning a transition out of full-time work, Nxdfamilyoffice provides the expert network to make it happen. From wealth management services and tax planning through to private banking and lifestyle advisory, every element of your financial life is managed with one priority: your long-term freedom. Consider it done.

FAQ

What is financial independence planning in simple terms?

Financial independence planning is the process of organising your finances so that your investments and assets generate enough income to cover your living expenses without needing to work. It involves budgeting, saving, investing, and managing debt towards a specific wealth target.

How do i calculate my financial independence number?

Multiply your expected annual expenses by 25. This figure, based on William Bengen’s 4% withdrawal rule, represents the portfolio size needed to sustain your lifestyle indefinitely when withdrawing 4% per year.

How long does it take to achieve financial independence?

The timeline depends almost entirely on your savings rate. Someone saving 50% of their income can reach FI in roughly 17 years from a standing start, while someone saving 10% may take 40 or more years.

What is the biggest risk in financial independence planning?

Inflation is the greatest long-term risk, as William Bengen himself has stated. Withdrawal rates must be adjusted annually to maintain purchasing power, and a plan that ignores inflation will erode your lifestyle over time.

Do i need a financial adviser for FI planning?

For straightforward finances, self-directed planning is viable. For high-net-worth individuals with complex assets, tax obligations, and estate considerations, professional private client services deliver material advantages that far outweigh the cost.

Recommended

- Lifestyle Assets for High-Net-Worth Clients – NXD Family Office

- Wealth Management Services – NXD Family Office

- Financial Services Tailored for High-Net-Worth Individuals – NXD Family Office

- Tax Advisory Services – NXD Family Office