Estate planning is the legal and financial process of organising, protecting, and transferring wealth according to your wishes. For newly wealthy families, the role of estate planning for new wealth is not optional. It is the foundation that determines whether your assets reach the right people, in the right form, at the right time.

Without a structured plan, newly acquired wealth is exposed to probate delays, creditor claims, misaligned inheritances, and unnecessary tax liabilities. The core instruments are wills, revocable trusts, durable powers of attorney, and healthcare directives. These documents, coordinated by an estate attorney and a qualified wealth advisor, form the baseline every newly wealthy family needs before anything else. Private wealth structuring sits directly alongside this process, ensuring assets are held in structures that match both your legal intentions and your tax position.

What is the role of estate planning for new wealth?

Estate planning for newly wealthy families starts with one clear task: getting organised. Comprehensive asset worksheets itemise every asset, its fair market value, its ownership structure, and the family members who will be affected by trust design and tax modelling. That single step prevents the most common and costly errors that follow a liquidity event.

Foundational estate planning documents include revocable trusts, wills, durable powers of attorney, healthcare directives, and beneficiary reviews. These form the baseline for newly wealthy families before any complex tax instruments are introduced. Skipping this stage and moving straight to sophisticated structures creates arrangements that are technically correct but practically unworkable.

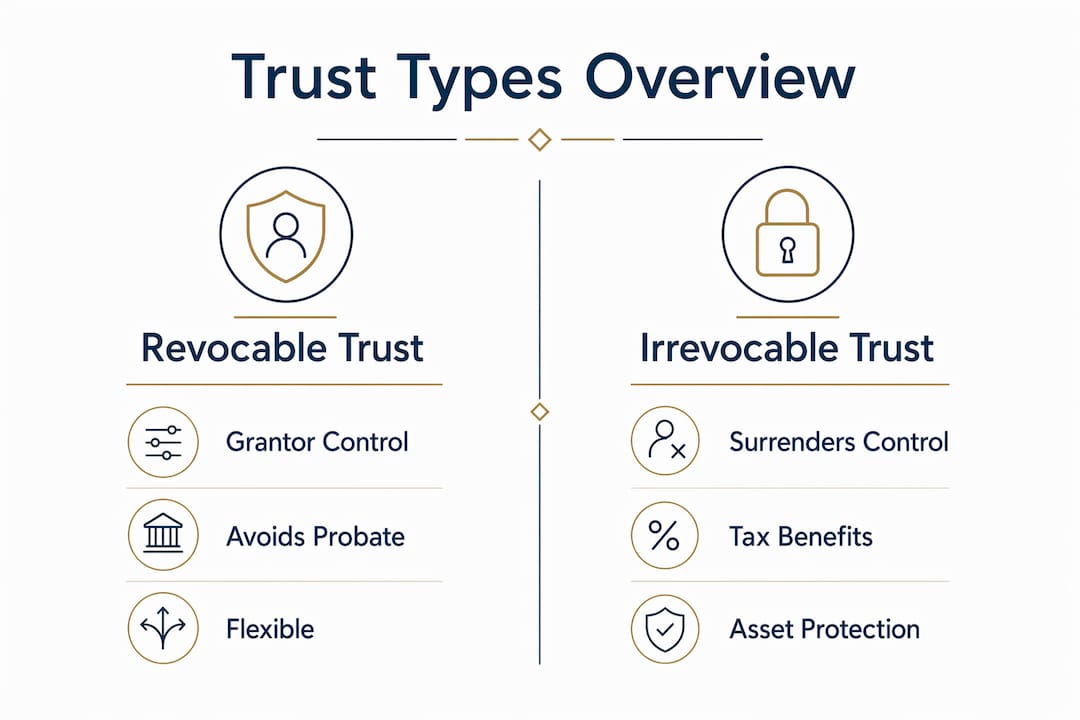

A revocable trust is the centrepiece of most new wealth plans. It avoids probate, keeps asset distribution private, and can be amended as circumstances change. A will covers assets that fall outside the trust. A durable power of attorney appoints someone to manage financial affairs if you become incapacitated. A healthcare directive records your medical wishes. Together, these four documents cover the vast majority of situations a newly wealthy family will face.

Beneficiary designation audits are equally critical at this stage. Retirement accounts, life insurance policies, and pension arrangements all pass outside a will or trust. If the named beneficiaries are outdated or misaligned with your estate plan, the distribution will not follow your intentions regardless of what your trust documents say.

Pro Tip: Start estate planning before or immediately after a liquidity event. Waiting until the dust settles means months of exposure with no legal protection in place.

How do advanced estate planning strategies support wealth growth?

Advanced estate planning strategies become relevant once foundational documents are in place and the estate trajectory is clear. Instruments such as Grantor Retained Annuity Trusts (GRATs), Spousal Lifetime Access Trusts (SLATs), and Intentionally Defective Grantor Trusts (IDGTs) each serve a specific purpose. GRATs transfer asset appreciation out of the estate at minimal gift tax cost. SLATs allow a spouse to benefit from trust assets while removing them from the taxable estate. IDGTs separate income tax from estate tax treatment, creating planning flexibility.

The decision to adopt these structures depends on three factors: the projected size of the estate, how much access you need to the assets, and your comfort with giving up control. The 2026 federal estate tax exemption stands at $15 million for individuals and $30 million for married couples. Families whose estates approach or exceed these thresholds have the most to gain from advanced planning. That threshold shapes the urgency and the choice of instrument.

The distinction between revocable and irrevocable trusts is central to this stage. Irrevocable trusts remove assets from grantor ownership, which provides creditor protection that revocable trusts cannot offer. The trade-off is control. Once assets are transferred into an irrevocable structure, you cannot simply take them back.

| Feature | Revocable trust | Irrevocable trust |

|---|---|---|

| Grantor control | Retained | Surrendered |

| Estate tax benefit | None | Significant |

| Creditor protection | Limited | Strong |

| Flexibility to amend | Yes | No |

| Probate avoidance | Yes | Yes |

Pro Tip: Do not adopt irrevocable structures until you have a clear picture of your liquidity needs. Locking assets away prematurely creates access problems that are expensive and sometimes impossible to reverse.

Why does asset titling and beneficiary alignment matter so much?

Correct asset titling is the step that most newly wealthy families overlook. A trust document alone does nothing. For a trust to avoid probate and function as intended, every relevant asset must be retitled in the trust’s name. Failing to do so leaves those assets subject to probate court, defeating the entire purpose of the structure.

The consequences are not just administrative. Probate is public, time-consuming, and costly. A family that has spent significant fees establishing a trust can still end up in court if the titling work was never completed. Real estate, bank accounts, brokerage accounts, and business interests all require specific retitling steps. Each asset type has its own process, and each must be handled correctly.

Beneficiary designations carry the same risk. Outdated designations on retirement and insurance accounts can silently sidestep trust arrangements, directing assets to the wrong people or creating unintended tax consequences. Regular audits are not a one-time task. They are an ongoing discipline, particularly after major life events such as marriage, divorce, the birth of a child, or the death of a named beneficiary.

Practical steps for maintaining alignment include:

- Maintain a master asset worksheet that records ownership structure, account numbers, and named beneficiaries for every asset.

- Review beneficiary designations on all retirement accounts and insurance policies at least every two years.

- Confirm that newly acquired assets are titled correctly at the point of purchase or transfer.

- Brief your estate attorney whenever a significant life event occurs, not just at scheduled reviews.

Pro Tip: Treat beneficiary designation reviews as a standing agenda item at your annual wealth review. One missed update can undo years of careful planning.

How does estate planning evolve as wealth and family needs change?

Estate planning is not a single event. It evolves as wealth grows, incorporating governance structures, tax strategies, and family education alongside the legal documents. Families that treat their estate plan as a living framework, rather than a filed document, consistently achieve better outcomes across generations.

The progression follows a clear sequence:

- Foundation stage. Establish core legal documents: revocable trust, will, powers of attorney, and healthcare directives. Complete the asset inventory and beneficiary audit.

- Alignment stage. Retitle assets into the trust. Confirm all beneficiary designations match the estate plan. Address any gaps in insurance coverage.

- Advanced strategy stage. Introduce irrevocable instruments where the estate size and tax position justify them. Engage a CPA to model the tax impact of each structure.

- Tax efficiency stage. Implement gifting strategies, charitable vehicles, and generation-skipping structures where appropriate. Coordinate with an insurance specialist on life insurance trust arrangements.

- Governance and legacy stage. Establish family governance frameworks, including family councils or investment policy statements. Begin educating the next generation on wealth stewardship.

Review frequency matters. A full estate plan review every five years is a reasonable baseline. Any major life event, including a business sale, inheritance, divorce, or significant change in tax law, should trigger an immediate review rather than waiting for the scheduled cycle.

Coordinated team workflows among estate attorneys, CPAs, insurance specialists, and wealth advisors are what prevent costly redesigns. Each professional covers a distinct area. When they work from the same asset inventory and family objectives, the plan holds together. When they work in isolation, gaps appear. Understanding what a family office does clarifies how this coordination is managed in practice for high-net-worth families.

Key takeaways

Effective estate planning for new wealth requires a staged approach, starting with foundational legal documents and evolving through advanced trust structures, precise asset titling, and coordinated professional oversight.

| Point | Details |

|---|---|

| Start with foundations | Establish a revocable trust, will, powers of attorney, and healthcare directives before any complex structures. |

| Audit beneficiaries regularly | Outdated designations on retirement and insurance accounts can override trust intentions entirely. |

| Retitle every asset | A trust document without correctly titled assets still leads to probate, defeating its core purpose. |

| Match structures to estate size | Advanced instruments like GRATs and SLATs are most valuable when the estate approaches tax exemption thresholds. |

| Coordinate your advisory team | Estate attorneys, CPAs, and insurance specialists must work from the same plan to avoid costly gaps. |

Why I believe most newly wealthy families plan too late and too fast

The two most common mistakes I see are not opposites. They are the same error expressed differently. Some families delay estate planning entirely, assuming they have time. Others rush straight into irrevocable trusts and complex gifting structures before the basics are in place. Both approaches create serious problems.

The families who delay are the ones who discover, after a health scare or a business dispute, that there is no will, no power of attorney, and no clear instruction for anyone. The families who move too fast often lock assets into structures they cannot access, or build technically correct arrangements that do not reflect how they actually want to live. Introducing advanced estate planning structures before foundational documents are properly established creates exactly this kind of impractical outcome.

What actually works is a sequenced approach with a coordinated team. The estate attorney handles the legal architecture. The CPA models the tax position. The wealth advisor holds the overall picture. No single professional can do all three well. Families that try to consolidate this into one relationship, often with a generalist adviser who has a financial interest in the products they recommend, end up with plans that serve the adviser’s interests rather than their own.

The most important thing a newly wealthy family can do is start with the basics, get them right, and then build. There is no shortcut that does not cost more later.

— Alex Goldstein

How NXD Family Office supports estate planning for new wealth

NXD Family Office works with newly wealthy individuals and families who need a coordinated, unbiased approach to protecting and managing their assets. The team connects clients with estate attorneys, CPAs, insurance specialists, and wealth advisors who work together from a single, clear picture of the client’s financial position and family objectives.

There are no referral fees and no commissions. Every recommendation is made in the client’s interest, not the adviser’s. For families who want their estate plan to hold together across generations, NXD Family Office provides the coordination that makes it possible. Speak to the team about wealth management services tailored to your family’s specific position and legacy goals.

FAQ

What are the first steps in estate planning for new wealth?

Foundational estate planning begins with a revocable trust, will, durable power of attorney, and healthcare directive, supported by a full asset inventory and beneficiary audit. These documents must be in place before any advanced structures are introduced.

When should newly wealthy families consider irrevocable trusts?

Irrevocable trusts become relevant when the estate approaches or exceeds tax exemption thresholds, currently $15 million per individual in 2026. The decision depends on estate size, access needs, and comfort with surrendering control over transferred assets.

Why do beneficiary designations matter in estate planning?

Beneficiary designations on retirement and insurance accounts override trust and will instructions entirely. Outdated or misaligned designations can direct assets to unintended recipients, making regular audits a non-negotiable part of any estate plan.

How often should an estate plan be reviewed?

A full review every five years is a standard baseline, but any major life event, including a business sale, marriage, divorce, or significant tax law change, should trigger an immediate review.

What professionals does an estate plan require?

Effective estate planning for inheritors and newly wealthy families requires an estate attorney, a CPA, an insurance specialist, and a wealth advisor working from the same asset inventory and family objectives. Coordination among these professionals prevents the gaps that lead to costly redesigns.