An independent financial advisor is defined as a professional who works solely for the client, with no institutional agenda and no commission from product sales. That distinction matters more than most families realise. When your wealth grows and your family’s needs become more complex, the difference between advice shaped by your interests and advice shaped by a bank’s product shelf becomes very costly indeed. Why families need independent advisors comes down to one core fact: you deserve guidance that is entirely on your side.

Why families need independent advisors, not bank advisors

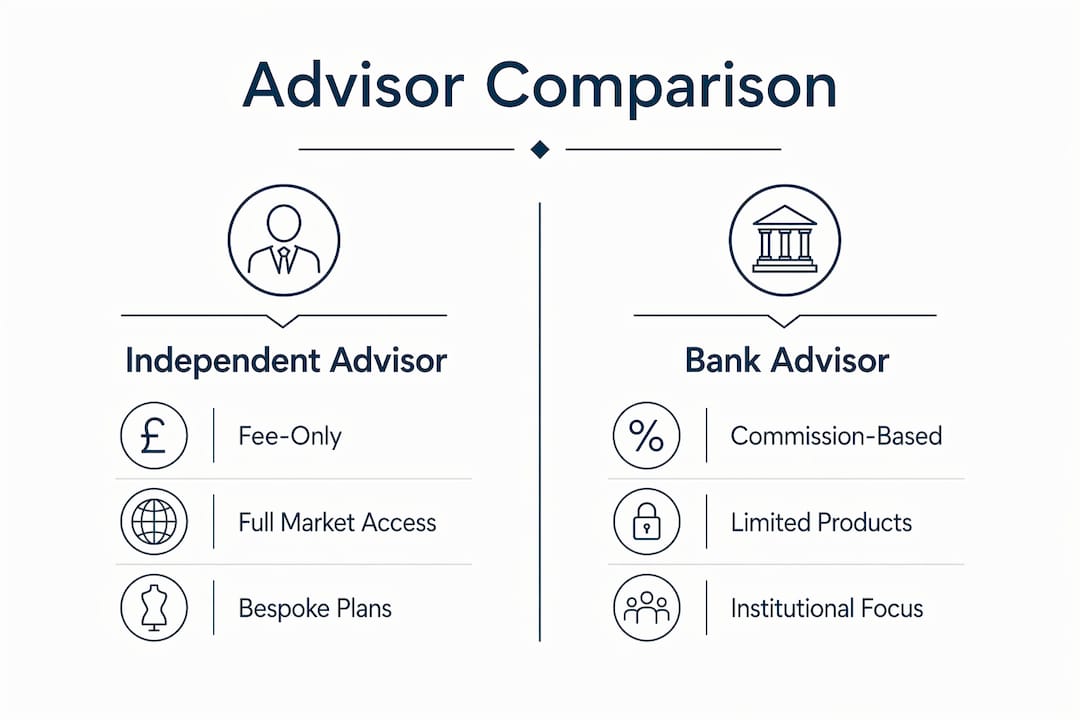

The fundamental difference between independent advisors and bank advisors is how they are paid. Fee-only independent advisors receive all compensation directly from the client, through flat fees, hourly charges, or assets-based fees. There is no commission. There is no incentive to recommend one product over another. That removes the single biggest source of conflict in traditional advisory relationships.

Bank advisors, by contrast, operate within institutional frameworks. They recommend from a set product shelf, and their compensation is often tied to what they sell. Families moving to independent firms shift from standardised product platforms to fully bespoke financial planning tailored to their unique goals. That is not a marginal improvement. It is a structural one.

The table below shows the core differences clearly.

| Factor | Bank or institutional advisor | Independent advisor |

|---|---|---|

| Compensation model | Commission or salary tied to products | Fee-only: flat, hourly, or assets-based |

| Product range | Limited to institutional shelf | Open architecture, full market access |

| Conflicts of interest | Structural conflicts present | Eliminated by design |

| Relationship continuity | Staff turnover is common | Single accountable advisor, often decades-long |

| Planning approach | Standardised products | Bespoke strategies for each family |

Continuity is a point that rarely gets enough attention. Independent, partner-owned firms offer a single accountable advisor who knows your family’s history, values, and goals over decades. Large banks rotate staff. That turnover means you regularly brief a new person on your circumstances, which costs time and erodes trust.

Pro Tip: Ask any prospective advisor directly: “How are you compensated, and will you put that in writing?” A genuinely independent advisor will answer without hesitation.

How do independent advisors tailor strategies for family wealth?

Bespoke family financial planning covers far more ground than selecting investments. A well-structured plan addresses cash flow, emergency reserves, insurance, debt, estate planning, and tax efficiency as a single connected picture. Yearly review of all these components is the standard for families with evolving needs, particularly those with self-employed members or cyclical income, who should maintain emergency reserves covering up to six months of expenses.

Independent advisors also access tax-efficient vehicles that banks rarely offer. Direct indexing, for example, allows families to own individual securities in an index rather than a fund, enabling precise tax-loss harvesting at the individual stock level. This is one of the tools that strategies at independent firms routinely include and that institutional platforms typically cannot provide.

Multi-generational planning is where independent advisors genuinely separate themselves. Involving younger family members early through structured family mapping builds cohesion and makes financial planning inclusive rather than opaque. Jeffrey Waller from Fidelity notes that this approach transforms planning from a transactional exercise into a tool for family unity. That matters enormously when wealth is being transferred across generations.

The components a thorough independent advisor addresses include:

- Cash flow analysis and budgeting across the whole family unit

- Emergency fund adequacy, reviewed annually

- Life, income protection, and liability insurance coverage

- Debt structure and repayment strategy

- Estate planning, wills, and lasting powers of attorney

- Tax planning, including direct indexing and trust structures

- Private investments and alternative assets

- Lending access and credit facilities for complex needs

A structured annual review process keeps all of these in alignment as the family’s circumstances change. A new business, a marriage, an inheritance, or a change in tax law can each shift the picture significantly. Independent advisors build that review into the relationship by design, not as an optional extra.

Pro Tip: Before your first meeting with an independent advisor, write down your family’s three most important financial goals for the next decade. Advisors who ask for this information unprompted are the ones worth keeping.

How to choose an independent advisor your family can trust

Selecting the right independent advisor requires more than checking credentials. Families should verify that a firm offers integrated financial planning, investment management, and lending services internally. A firm that handles complex needs through referrals to third parties introduces the same conflicts of interest that independent advice is supposed to eliminate.

The practical checklist for vetting an advisor covers several areas:

- Fee transparency. Ask for a written breakdown of all fees before signing anything.

- Fiduciary status. Confirm the advisor is legally obligated to act in your best interests at all times.

- Service breadth. Check whether the firm handles lending, insurance, and estate planning directly or outsources these.

- Advisor continuity. Ask who your primary advisor will be and what happens if they leave.

- Client references. Request introductions to existing clients with similar family profiles.

- Regulatory standing. Verify registration with the Financial Conduct Authority (FCA) in the UK.

The full advisory model matters most for families with complex or ultra-high net worth needs. A firm that can handle credit access directly, without routing you to a third-party bank, gives you faster decisions and keeps your financial picture in one place. For families managing private investments, business interests, and lifestyle assets simultaneously, that integration is not a luxury. It is a necessity.

The most common mistake families make is selecting an advisor based on personality alone. Rapport matters, but it cannot substitute for structural independence, fee transparency, and proven service breadth. Use the family financial management checklist as a starting framework before your first advisory meeting.

Pro Tip: Run a quick FCA register check on any advisor before your first meeting. It takes two minutes and confirms they are authorised to give financial advice in the UK.

What are the most common myths about independent advisors?

The most persistent myth is that independent means limited. Families sometimes assume that stepping away from a large bank means losing access to sophisticated products or specialist expertise. The opposite is true. Client-centric independence enables advisors to access the full market rather than a curated institutional shelf. Shirl Penney, CEO of Dynasty Financial Partners, describes independence as what allows advisors to prioritise families as their core business, free from bureaucratic constraints.

A second myth is that independent advice costs more. Fee-only structures are transparent by design. You know exactly what you pay and what you receive. Commission-based advice, by contrast, embeds costs inside product charges that are rarely itemised. Families often pay more through institutional models without realising it.

The third myth is that independent advisors are harder to access or less established. Client demand for independence is growing, driven by generational wealth transfer and rising expectations for personalised guidance. The independent advisory sector has grown significantly in response. Families now have access to well-resourced, specialist independent firms that rival the service depth of any private bank.

The benefits of independent advisors are concrete, not theoretical. They include unbiased advice, transparent costs, bespoke planning, and a relationship built entirely around your family’s interests. The importance of financial advisors who operate without conflicts of interest cannot be overstated when the decisions in question affect multiple generations.

Key takeaways

Independent financial advisors deliver unbiased, bespoke guidance because their fee-only model removes conflicts of interest and aligns every recommendation with the family’s goals.

| Point | Details |

|---|---|

| Fee-only model removes conflicts | Independent advisors earn from clients directly, eliminating commission-driven product bias. |

| Bespoke planning covers all needs | Strategies address cash flow, tax, insurance, estate planning, and private investments as one plan. |

| Advisor continuity builds trust | Partner-owned independent firms offer decades-long relationships, unlike high-turnover bank teams. |

| Vet for the full advisory model | Choose firms that handle planning, investment, and lending internally for complex family needs. |

| Independence is not a limitation | Fee-only advisors access the full market and often deliver more for less than institutional models. |

Why I believe continuity is the real differentiator

The conversation about independent advisors tends to focus on fees and conflicts of interest. Both matter. But in my experience, the factor that most consistently determines whether a family thrives financially over generations is continuity of relationship.

Families are not static. A business sale, a divorce, a child’s education abroad, a parent’s care needs — each of these changes the financial picture in ways that require an advisor who already knows the full context. When that advisor has been with the family for ten or fifteen years, the quality of the advice is categorically different. They are not starting from a briefing document. They are drawing on lived knowledge of what the family values, what they fear, and what they have already been through.

The most successful families use continuous, personalised advisory relationships to navigate complex financial changes across generations. That is not a coincidence. It is the direct result of choosing advisors whose business model rewards long-term client relationships rather than short-term product sales.

What I find most frustrating about traditional institutional advice is not the fees. It is the churn. Families build trust with an advisor, and then that person moves on or is reassigned. The relationship resets. The family loses the accumulated understanding that took years to build. Independent firms, structured around partner ownership and client continuity, solve this problem by design. That is the argument I return to every time a family asks me whether independence is worth it. It always is.

— Alex Goldstein

NXD Family Office: bespoke wealth management for your family

NXD Family Office works with high-net-worth families who expect more than a standard advisory relationship. The firm provides independent guidance across wealth management, insurance, private investments, and lifestyle assets, with no referral fees and no commissions. Every recommendation is made solely in the client’s interest.

For families seeking a trusted partner to manage complex financial needs across generations, NXD Family Office offers personalised wealth management services built around your goals, not a product shelf. Whether you are planning a generational transfer, restructuring your assets, or simply want advice you can trust completely, the team is ready. For families who want to understand the full scope of what independent guidance looks like, the vetting wealth advisors guide is a practical starting point. Consider it done.

FAQ

What is an independent financial advisor?

An independent financial advisor is a professional who provides financial guidance without ties to any institution or product provider. They operate under a fee-only model, meaning all compensation comes directly from the client, with no commissions.

Why choose an independent advisor over a bank advisor?

Independent advisors offer bespoke strategies, full market access, and no conflicts of interest. Bank advisors are limited to institutional product shelves and are often compensated through commissions that can influence their recommendations.

How do independent advisors help with family financial planning?

Independent advisors build comprehensive plans covering cash flow, tax efficiency, estate planning, insurance, and multi-generational wealth transfer. They conduct annual reviews to keep strategies aligned with the family’s evolving circumstances.

What does a fee-only advisor actually cost?

Fee-only advisors charge through flat fees, hourly rates, or a percentage of assets under management. All fees are disclosed upfront, making the total cost transparent and comparable, unlike commission-based models where charges are embedded in product pricing.

How do I know if an independent advisor is trustworthy?

Verify FCA registration, confirm fiduciary status in writing, and ask whether the firm handles planning, investment, and lending internally. Requesting references from existing clients with similar family profiles is also a reliable way to assess credibility before committing.