Philanthropic wealth planning is defined as the deliberate integration of charitable giving into your overall wealth management strategy, structured to maximise both social impact and financial efficiency. For high net worth individuals and families in the UK, this goes well beyond writing a cheque to a favoured cause. It means aligning your charitable goals with estate planning, tax strategy, and succession objectives to build a lasting legacy. Key vehicles include donor-advised funds (DAFs), charitable trusts, and direct asset gifting. The UK tax framework, governed by HMRC and overseen by the Charity Commission, provides meaningful incentives that make philanthropic financial planning one of the most financially rational decisions a wealthy family can make.

What is philanthropic wealth planning and how does it work?

Philanthropic wealth planning operates through two broad approaches: giving during your lifetime and giving through your estate. Each carries distinct tax consequences and requires different structures. The choice between them shapes how much control you retain, how much tax you save, and what legacy you leave.

Lifetime giving allows you to see your charitable impact directly. You can donate cash, shares, or property to registered charities and receive immediate Income Tax and Capital Gains Tax relief. Giving through your estate, typically via a will, can reduce the Inheritance Tax (IHT) burden on your beneficiaries. Leaving 10% or more of your net estate to charity reduces the IHT rate from 40% to 36%. That 4% reduction on a large estate represents a substantial saving, often running into hundreds of thousands of pounds.

The main philanthropic vehicles available in the UK are:

- Direct donations to registered charities, qualifying for Gift Aid and Income Tax relief

- Donor-advised funds (DAFs), which pool contributions and allow flexible grantmaking over time

- Charitable trusts, which offer full donor control but require Charity Commission registration

- Asset gifting, including shares and property, which can eliminate Capital Gains Tax liabilities

Pro Tip: Gifting appreciated shares directly to a charity rather than selling them first avoids Capital Gains Tax entirely and qualifies for Income Tax relief on the full market value. This is one of the most under-used tactics in charitable wealth management.

Charitable giving integrated with wills, succession plans, and asset protection prevents unintended consequences for other beneficiaries. Philanthropy works best when it sits inside your wider estate plan, not alongside it.

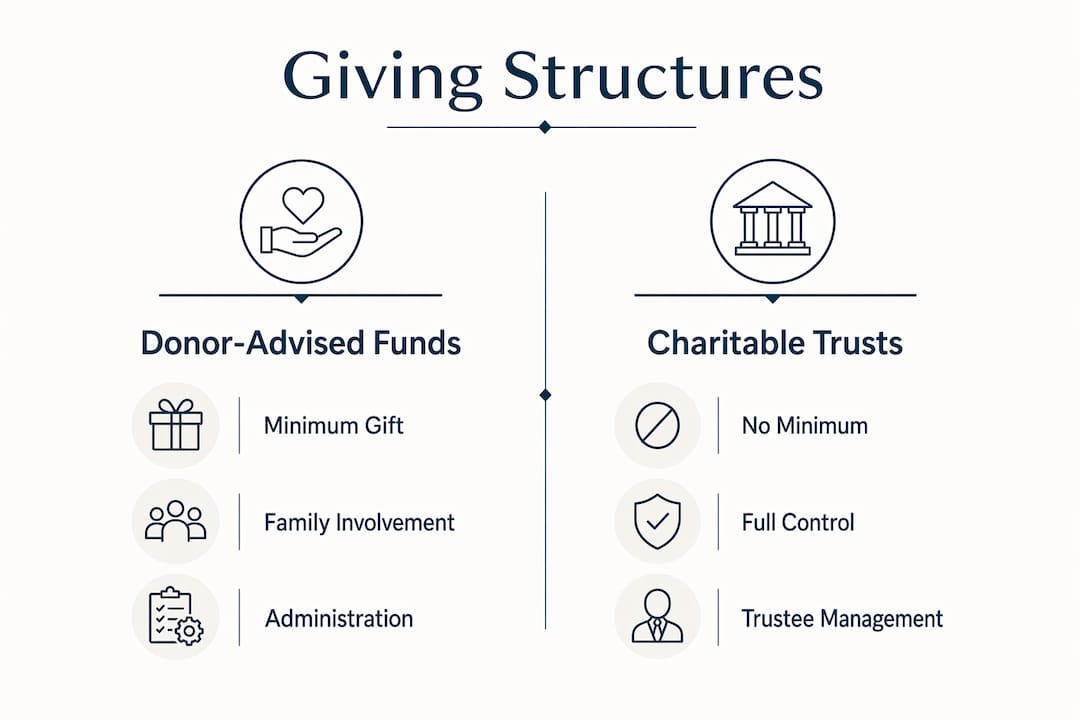

Donor-advised funds and charitable trusts: which suits you?

The two most commonly used structures in UK philanthropic wealth planning are donor-advised funds and charitable trusts. They serve similar purposes but differ sharply in governance, cost, and control.

A donor-advised fund is a giving account held within a sponsoring charity. You make an irrevocable contribution, receive immediate tax relief, and then recommend grants to causes over time. DAFs typically require a minimum opening contribution of £250,000, with subsequent donations of at least £2,000. Funds over £500,000 may access bespoke investment options. The sponsoring charity manages all compliance and investment decisions, making DAFs a genuinely light-touch option for donors who want flexibility without administrative burden.

A charitable trust, by contrast, places you or your appointed trustees in full control. You set the charitable objectives, appoint trustees, register with the Charity Commission, and manage ongoing governance and reporting. Charitable trusts require full Charity Commission registration and trustee duties, and the administrative burden deters roughly 22% of high net worth individuals who prefer simpler options. The upside is permanence: a charitable trust can exist in perpetuity under UK law, unlike private trusts which are limited to 125 years.

| Feature | Donor-advised fund | Charitable trust |

|---|---|---|

| Minimum contribution | £250,000 | No fixed minimum |

| Control level | Advisory only | Full trustee control |

| Administrative burden | Low (sponsor manages) | High (trustee duties) |

| Charity Commission registration | Not required | Required |

| Perpetual existence | No | Yes |

| Tax relief on contribution | Immediate | Immediate |

| Suited to | Flexible, family giving | Legacy, named cause |

DAFs enable ongoing family involvement and flexible grantmaking, which makes them well suited to families whose philanthropic interests evolve over time. Charitable trusts suit donors with a specific, long-term cause and the appetite to manage governance properly.

Pro Tip: If you want your children or grandchildren involved in giving decisions without the legal weight of trusteeship, a DAF is the cleaner route. It builds philanthropic values across generations without the compliance overhead.

Tax implications of philanthropic wealth planning in the UK

The UK tax system rewards charitable giving at multiple levels. Understanding each relief helps you structure giving to achieve the greatest combined financial and social benefit.

The most significant estate planning benefit is the IHT reduction. The nil-rate band has been frozen at £325,000 since 2009 and will remain so until at least april 2031. The Residence Nil Rate Band adds up to £175,000 per person, subject to restrictions. With property values rising and thresholds frozen, more estates fall into IHT territory each year. Donating 10% or more of the net estate to charity cuts the IHT rate from 40% to 36%, a meaningful saving on any substantial estate.

Capital Gains Tax relief is equally compelling. Donating appreciated assets such as shares, property, or business interests directly to charity eliminates the CGT liability that would arise from a sale. You also receive Income Tax relief based on the full market value of the asset. This makes asset gifting considerably more tax-efficient than selling the asset and donating the cash proceeds.

| Tax | Lifetime giving benefit | Estate giving benefit |

|---|---|---|

| Inheritance Tax | Reduces taxable estate | Reduces IHT rate to 36% with 10%+ gift |

| Capital Gains Tax | Eliminated on gifted assets | N/A |

| Income Tax | Relief on cash donations via Gift Aid | N/A |

Philanthropy enhances both social impact and financial outcomes when properly integrated into estate planning. The tax reliefs are not incidental. They are a core reason why charitable wealth management belongs at the centre of any serious estate plan, not as an afterthought.

Practical steps to build your philanthropic giving strategy

Starting philanthropic wealth planning requires a clear assessment of your financial position before selecting any structure or vehicle.

-

Value your estate accurately. Understand your total assets, liabilities, and projected IHT exposure. This gives you a baseline for deciding how much to allocate to charitable giving without compromising family financial security.

-

Define your philanthropic objectives. Identify the causes, geographies, and outcomes that matter to you and your family. Clarity here determines whether a DAF, charitable trust, or direct giving suits you best.

-

Select the right giving vehicle. Match your chosen structure to your appetite for control, administrative involvement, and legacy goals. A DAF suits most families starting out. A charitable trust suits those with a defined, long-term mission.

-

Engage specialist advisors. Professional estate planners evaluate charitable giving strategies to ensure tax optimisation across Income Tax, CGT, and IHT alongside your philanthropic ambitions. This is not a task for a generalist accountant.

-

Involve your family. Shared philanthropic values strengthen family cohesion and ensure the giving strategy endures across generations. Bring adult children into the conversation early.

-

Review regularly. Tax law changes, family circumstances shift, and charitable interests evolve. A philanthropic plan that is not reviewed becomes misaligned within a few years.

The most common pitfall is treating philanthropy as a standalone decision. Integrating charitable giving with estate liquidity, care needs, and succession planning prevents unintended consequences for other beneficiaries and preserves family harmony.

Pro Tip: Ask your advisor to model the IHT saving from a 10% charitable gift against the cost of that gift to your estate. For many families, the net financial impact on beneficiaries is neutral or positive, which makes the philanthropic case straightforward.

Key takeaways

Philanthropic wealth planning is most effective when charitable giving is built into your estate plan from the outset, not added as an afterthought.

| Point | Details |

|---|---|

| Core definition | Philanthropic wealth planning aligns charitable giving with estate, tax, and succession strategy. |

| IHT reduction | Donating 10% or more of your net estate cuts the IHT rate from 40% to 36%. |

| DAFs vs charitable trusts | DAFs offer simplicity and flexibility; charitable trusts offer full control and permanence. |

| Asset gifting advantage | Gifting appreciated shares or property to charity eliminates CGT and qualifies for Income Tax relief. |

| Professional advice is essential | Specialist advisors ensure giving structures align with your full tax and estate position. |

Why I think most wealthy families leave philanthropy too late

The most consistent pattern I see among high net worth clients is that philanthropy gets treated as a reward for financial success rather than a component of the plan itself. Families wait until the estate is “sorted” before thinking about giving. By that point, the most tax-efficient windows have often closed.

The families who get this right start the conversation early, sometimes decades before they expect to need it. They treat charitable giving as part of estate planning for new wealth, not a separate exercise. The result is a plan where the tax reliefs compound over time, the family develops shared values around giving, and the legacy is genuinely meaningful rather than a last-minute gesture.

The other misconception I encounter regularly is that charitable trusts are always the “serious” option and DAFs are for people who cannot commit. That is simply wrong. A well-structured DAF, with family members involved in grant recommendations, can be every bit as purposeful as a trust, with a fraction of the governance burden. The right structure is the one your family will actually use and sustain.

Philanthropy is not generosity dressed up in tax planning. It is a deliberate choice to direct wealth toward outcomes you care about, in the most financially rational way possible. The families who treat it that way build legacies that outlast them.

— Alex Goldstein

How NXD Family Office supports philanthropic wealth planning

Philanthropic wealth planning sits at the intersection of tax law, estate strategy, and personal values. Getting it right requires advisors who understand all three, and who have no financial incentive to push one structure over another.

NXD Family Office works with high net worth individuals and families to build giving strategies that are genuinely aligned with their financial position and legacy goals. The team provides access to specialist tax advisory services covering IHT planning, CGT mitigation, and charitable structure selection, all without referral fees or commissions. Every recommendation reflects what is right for the client, not what generates the highest fee for the advisor. If you want to understand how philanthropy fits into your wider wealth plan, NXD Family Office can show you exactly where the opportunities lie.

FAQ

What is philanthropic wealth planning?

Philanthropic wealth planning is the structured integration of charitable giving into your wealth management and estate planning strategy. It uses vehicles such as donor-advised funds, charitable trusts, and asset gifting to maximise both social impact and tax efficiency.

How does charitable giving reduce inheritance tax in the UK?

Leaving 10% or more of your net estate to charity reduces the UK IHT rate from 40% to 36%. With the nil-rate band frozen at £325,000 until at least april 2031, this relief is increasingly valuable for larger estates.

What is the difference between a donor-advised fund and a charitable trust?

A donor-advised fund is managed by a sponsoring charity, requires minimal administration from the donor, and typically needs a minimum opening contribution of £250,000. A charitable trust gives the donor full control but requires Charity Commission registration and ongoing trustee governance.

Can I donate assets other than cash to charity?

Yes. Donating appreciated assets such as shares or property directly to a charity eliminates Capital Gains Tax on the gain and qualifies for Income Tax relief based on the full market value, making it more tax-efficient than a cash donation.

When should I start philanthropic wealth planning?

The earlier the better. Integrating charitable giving into your estate plan from the outset allows tax reliefs to compound over time and gives your family the opportunity to build shared philanthropic values across generations.